Northrop Grumman Q1 2026 Performance Analysis

Date published: 28 April 2026

Event date: 21 April 2026

Event location / region: Falls Church, Virginia, United States / US defence industrial base

Event: Northrop Grumman Q1 2026 earnings release and investor call

Northrop Grumman opened 2026 with solid organic growth, stronger margins, a near-record backlog and a clear message to shareholders: demand is strong, guidance is intact, and the company is investing to scale production around the Pentagon’s highest-priority programmes.

The company reported Q1 2026 sales of $9.9 billion, up 4% year-on-year, with organic sales up 5%. Net earnings rose to $875 million, while diluted earnings per share increased to $6.14, compared with $3.32 in Q1 2025. Operating income reached $989 million, with an operating margin of 10.0%.

At first glance, this is a strong financial quarter. But the numbers need context. A large part of the year-on-year profit improvement comes from the absence of the $477 million B-21 loss provision recorded in the prior-year quarter. In other words, Northrop’s Q1 2026 results show better performance, but also benefit from an easier comparison base.

The more important message is not only in the income statement. It is in the order book and in the company’s production plans.

Northrop recorded $9.8 billion in net awards during the quarter and ended Q1 with a backlog of $95.6 billion. Significant new awards included restricted programmes, F-35 work, infrared countermeasures programmes and Triton. This gives the company strong visibility into future revenue and supports management’s confidence in its 2026 outlook.

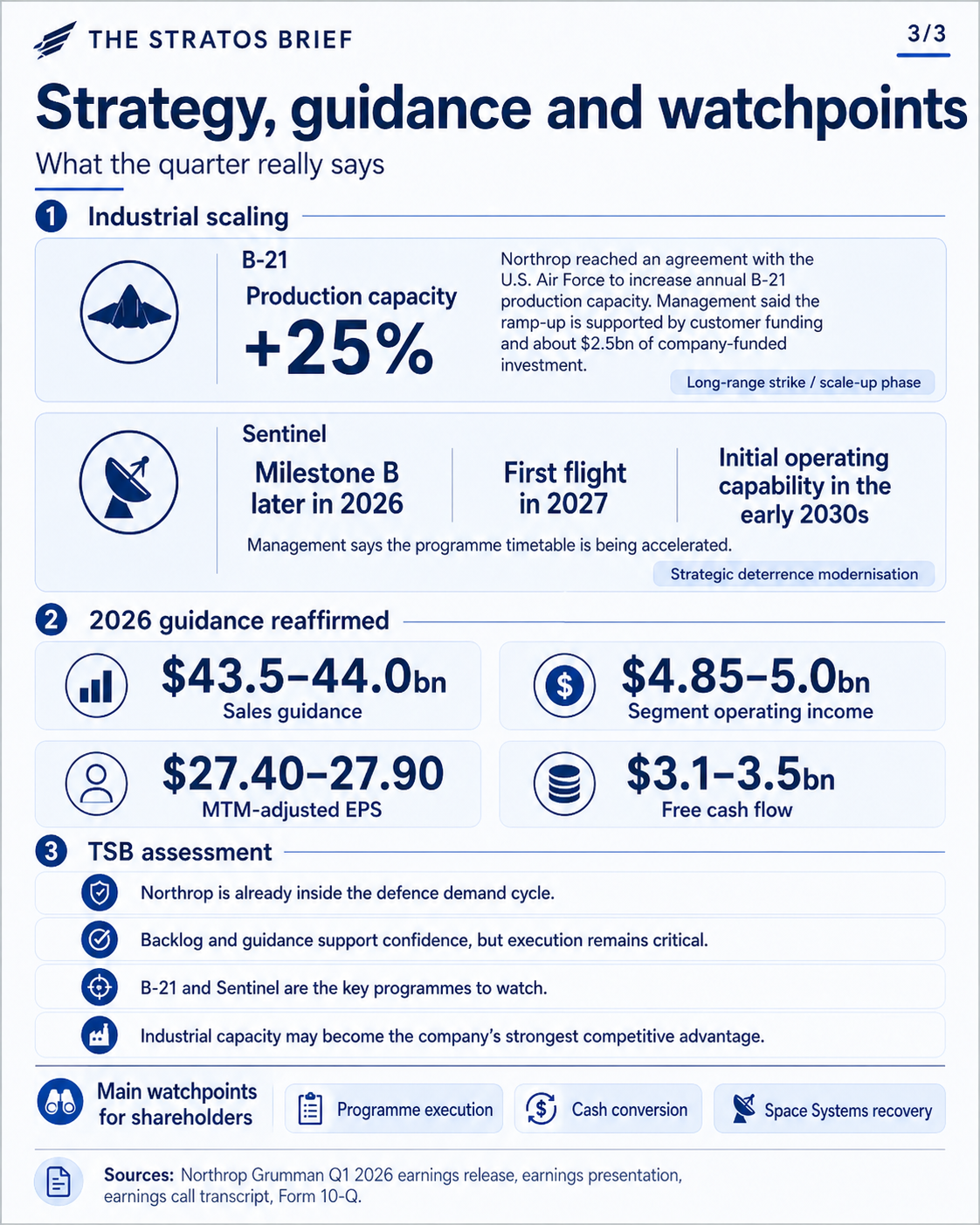

The company also reaffirmed its full-year 2026 guidance. It expects sales of $43.5–44.0 billion, segment operating income of $4.85–5.0 billion, MTM-adjusted EPS of $27.40–27.90, and free cash flow of $3.1–3.5 billion.

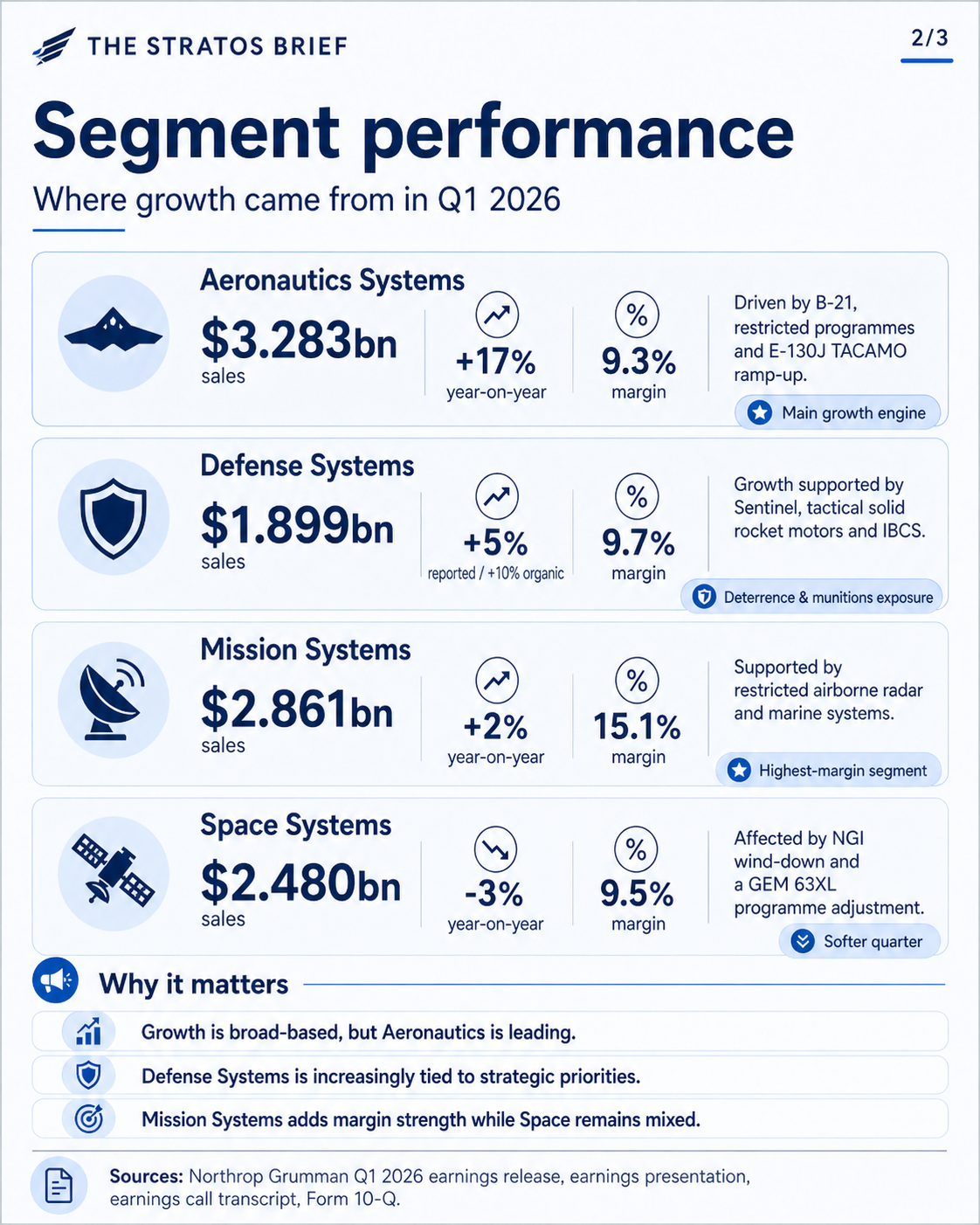

Segment performance tells the real story.

Aeronautics Systems was the main growth engine. Sales increased 17% to $3.3 billion, driven by the B-21, other restricted programmes and the ramp-up of the E-130J TACAMO programme. The segment moved from a loss in Q1 2025 to an operating margin of 9.3% in Q1 2026. This was mainly due to the absence of the prior-year B-21 loss provision.

The B-21 was also the most important strategic item in the quarter. Northrop reached an agreement with the US Air Force to increase annual B-21 production capacity by 25%. Management said the ramp-up will be supported by customer funding and around $2.5 billion of company-funded investment, mainly in new facilities. This is not just a programme update. It suggests that the B-21 is moving deeper into the industrial scaling phase.

Defense Systems grew more modestly on a reported basis, with sales up 5% to $1.9 billion. However, organic sales increased 10%, helped by the Sentinel programme, tactical solid rocket motors and the Integrated Battle Command System portfolio. This is strategically important because these areas are directly linked to nuclear deterrence modernisation, munitions demand, air and missile defence, and the wider need to expand defence production capacity.

Sentinel was another major theme. Management said it is working with the US Air Force to accelerate the programme, with Milestone B expected later this year, first flight in 2027 and initial operating capability in the early 2030s. Sentinel is already delivering double-digit growth for Northrop and is expected to remain one of the company’s important long-term growth drivers.

Mission Systems remained the strongest margin performer. Sales increased 2% to $2.9 billion, while operating income increased 20%. The segment delivered a 15.1% operating margin, supported by restricted airborne radar programmes, marine systems and more favourable earnings adjustments. This part of the business remains important because it sits close to the sensors, radars, electronic systems and command-and-control capabilities that underpin modern networked warfare.

Space Systems was the weaker part of the quarter. Sales fell 3% to $2.5 billion, and operating income declined 17%. The main reasons were the wind-down of work on the Next Generation Interceptor programme and a $71 million unfavourable adjustment on the GEM 63XL programme after a launch anomaly. This does not mean the whole space portfolio is weak, but it shows that the segment remains exposed to programme timing, technical risk and contract-level adjustments.

Cash flow was broadly in line with the prior year. Northrop reported free cash flow of negative $1.8 billion in Q1, similar to Q1 2025. Management described this as consistent with the company’s usual cash flow pattern, with stronger cash generation expected later in the year. The company also ended the quarter with more than $2 billion of cash on the balance sheet.

The wider strategic picture is clear. Northrop is increasingly shaped around programmes that match the current direction of US defence priorities: strategic deterrence, long-range strike, missile defence, solid rocket motors, restricted programmes, advanced sensors and space systems.

Management also emphasised demand for solid rocket motors, smart munitions, ammunition and tactical missiles. It said the company’s weapons business is nearing 10% of total company sales and is positioned to grow faster than the company average. Missile defence is also approaching 10% of company sales. These are not marginal business lines anymore. They are becoming central to Northrop’s growth story.

For shareholders, the message from the reporting event was therefore relatively clear: Northrop is not presenting itself as a turnaround story. It is presenting itself as a defence prime with a large backlog, improving margins, strong exposure to US strategic priorities and a willingness to invest capital into production capacity.

The risks remain. B-21 and Sentinel are complex, high-value programmes. Space Systems had a softer quarter. The company still depends heavily on US government budgets, programme timing, supplier performance and execution discipline. Higher capital expenditure also means that management must prove that today’s investment will convert into future revenue, margin and cash.

Still, compared with Boeing’s recent story of recovery and stabilisation, Northrop’s Q1 reads differently. This is a company already positioned inside the demand cycle. The question is not whether demand exists. The question is how fast Northrop can turn that demand into production, deliveries and cash.

TSB assessment: Northrop Grumman’s Q1 2026 results show a defence company with steady growth, stronger margins, a deep backlog and strong exposure to the areas where Washington is increasing urgency: strategic deterrence, long-range strike, missile defence, munitions, sensors and space. The quarter was helped by easier comparison against last year’s B-21 charge, but the underlying message is still important. Northrop is investing for scale, and in the current security environment, industrial capacity may become one of the most important competitive advantages in the defence sector.

Sources

Northrop Grumman Q1 2026 Earnings Release, April 21, 2026.

Northrop Grumman Q1 2026 Earnings Call Transcript, April 21, 2026.

Northrop Grumman Q1 2026 Conference Call Presentation.

Northrop Grumman Form 10-Q for the quarter ended March 31, 2026.